Volatility Check in Returns charts

Hi All! In our previous tutorial, we had introduced stylized facts, what the five stylized facts are and had also covered stylized fact 1 – Distribution of returns – Is it non-Gaussian? In this tutorial, we will be covering stylized fact 2 – “Are Volatility clusters formed in returns chart?” and do Volatility Check in Returns charts using Python. New to this series? – Go to part 1 of Financial Analytics series to develop a good understanding on this.

Stylized Fact 2: Volatility Check in Returns charts

Let’s choose MSFT stock for our analysis. We’ll use yfinance to fetch stock data of MSFT.

# Importing the libraries

import pandas as pd

import yfinance as yf

import numpy as np

import matplotlib.pyplot as plt

# Downloading MSFT data from yfinance from 1st January 2010 to 31st March 2020

msftStockData = yf.download( 'MSFT',

start = '2010-01-01',

end = '2020-03-31',

progress = False)

# Checking what's in there the dataframe by loading first 5 rows

msftStockData.head()

# Checking what's in there the dataframe by loading last 5 rows

msftStockData.tail()

# Calculating log returns and obtaining column to contain it

msftStockData['Log Returns'] = np.log(msftStockData['Adj Close']/msftStockData['Adj Close'].shift(1))

# Checking what's in there the dataframe by loading first 5 rows

msftStockData.head()

# Using back fill method to replace NaN values

msftStockData['Log Returns'] = msftStockData['Log Returns'].fillna(method = 'bfill')

msftStockData.head()

# Line chart of log return series

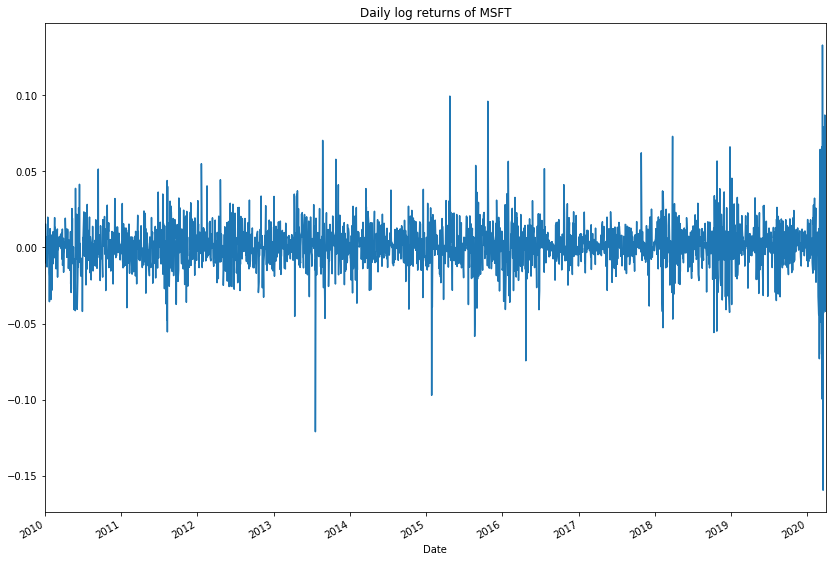

msftStockData['Log Returns'].plot(title = 'Daily log returns of MSFT', figsize = (14,10))

Thus, we can see that volatility clusters are formed in the line chart – there are some periods having higher returns and some periods have lower returns and they alternate forming a cycle of high-low-high. Thus, volatility doesn’t remain the same always.

So guys, we have just now explored Stylized fact 2 in this tutorial. In the next tutorial, we will explore stylized fact 3. Stay tuned! And don’t forget to subscribe to our YouTube channel.

One thought on “Volatility Check in Returns charts: FA9”